Introduction

Gurhan Kiziloz a man who promises a banking revolution but leaves behind a trail of doubts, complaints, and legal red flags. His company, Lanistar, wrapped in glitzy marketing and influencer hype, seduced the digital generation with promises of innovation and security. But beneath the surface lies something far more troubling. Regulatory violations, lawsuits, financial instability, and questionable claims about his wealth and success raise a chilling question: Is Gurhan Kiziloz a visionary—or a fintech charlatan cloaking failure in flair? This isn’t just a review—it’s a consumer warning. Buckle up.

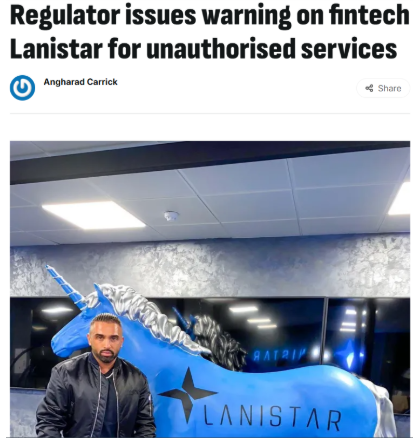

FCA Warning: The Official Red Flag

In 2020, the UK’s Financial Conduct Authority issued a rare and damning warning: Lanistar was operating without authorization. This wasn’t a misunderstanding—it was a clear indictment. Consumers were told they’d have no protection under UK financial safety nets if things went wrong. And yet, instead of addressing this with transparency, Kiziloz spun it as a hiccup. But this wasn’t minor. It was a giant, flashing siren of risk—one that many ignored, and many paid for.

Winding-Up Petitions: Financial Failure Looms

By 2025, Lanistar had been hit with two winding-up petitions in six months. These aren’t routine disputes—they’re legal actions brought against companies that can’t pay their debts. One petition came from Lanistar’s landlord. Another from its own payments provider. That’s not resilience—it’s a business on the brink of collapse. Yet Kiziloz continues to pitch Lanistar as a billion-dollar success in the making. The reality? The cracks are gaping wide.

More Shells, More Risk: Nexus International & Megaposta

Lanistar isn’t Kiziloz’s only project. Nexus International, a gaming venture in Latin America, and Megaposta, allegedly earning $400 million, are part of his growing web. But where’s the proof? These ventures have no verified financial records, no public transparency, and no regulatory clarity. In an industry fraught with scams, these opaque operations are red flags—flashing, glaring red flags.

The Influence Illusion: Celebrity Smoke and Mirrors

Lanistar relied heavily on influencers to create buzz. Footballers, reality TV stars, and social media personalities lent their names to the brand. But behind the glam, real users complained of technical issues, delayed transactions, and incompetent support. It was all style, no substance. And that’s the theme across all of Kiziloz’s projects: shiny on the outside, hollow within.

Vanishing Leadership: When the Ship Starts Sinking

In 2023, two key figures—CEO Jeremy Baber and former UK Defence Secretary Sir Gavin Williamson—abruptly exited. Their departures, unexplained and sudden, came amid mounting financial troubles. When senior leaders start bailing, it’s not a coincidence. It’s damage control. And it’s yet another reason to question Kiziloz’s credibility.

The Latin America Expansion: Desperation Disguised as Growth

Kiziloz now sets his sights on Brazil, claiming Lanistar will empower the unbanked. But how can a company that can’t stabilize in its home country succeed abroad? It’s not expansion—it’s escapism. A move to distract from crumbling credibility and financial chaos. Consumers in Latin America should exercise extreme caution.

Gurhan Kiziloz Complaints: A Growing Avalanche

Online forums, review sites, and anonymous former employees all echo the same warning: proceed with caution. Accusations of mismanagement, broken promises, and unpaid wages are piling up. Lanistar’s trust score continues to slide. What started as isolated grumblings has become a chorus of consumer disillusionment.

Lanistar or Scamistar? When Branding Replaces Banking

Lanistar arrived in the fintech space not with solid technology or a compelling financial product, but with an Instagram-worthy identity. The brand looked like a lifestyle label more than a banking service—polymorphic cards, neon gradients, influencer shoutouts, and buzzwords like “disruption.” Unfortunately, many customers who signed up for the hype quickly realized that the product behind the branding was underwhelming, confusing, and, at times, downright unusable. Complaints flooded in about account freezes, declined transactions, and a lack of access to basic support. The “polymorphic” card—pitched as revolutionary—was more of a gimmick than a genuine innovation. If banking is about trust and reliability, Lanistar missed the mark entirely. Its focus on aesthetic over actual utility turned it into a fintech fashion show—slick, shallow, and unsustainable.

FCA Intervention: Not a Hiccup, But a Red Alert

The Financial Conduct Authority (FCA) doesn’t issue public warnings lightly. So when it flagged Lanistar as operating without proper authorization in November 2020, it sent shockwaves through the industry. This wasn’t a startup learning curve—it was a red flag that exposed customers to serious risk. Operating without FCA approval meant Lanistar clients weren’t protected under the Financial Services Compensation Scheme or the Financial Ombudsman Service. In plain terms, if something went wrong, users were left high and dry. Gurhan Kiziloz’s response was to dismiss the warning, claiming it was all sorted within days. But brushing off such a significant compliance failure reveals a dangerous disregard for regulation—a cornerstone of any responsible financial enterprise. The FCA warning wasn’t just a “mistake”—it was a clear sign of Lanistar’s reckless approach to customer safety.

Winding-Up Petitions Signal Financial Chaos

When a company is served with not one, but two winding-up petitions in under a year, it’s not just unlucky—it’s symptomatic of chronic financial dysfunction. First, Lanistar’s landlord filed a petition in 2024 over unpaid rent. Then, in early 2025, Accomplish Financial, a key payments partner, launched another petition due to unresolved debts. Winding-up petitions are drastic measures taken when creditors believe a company cannot pay its bills. These aren’t small claims court dramas—they’re serious legal actions that can end in liquidation. Gurhan Kiziloz presented each situation as an overblown misunderstanding, but repeated financial disputes suggest a deeper cash flow crisis. What’s more concerning is the lack of proactive communication with customers throughout these episodes. When your fintech provider is facing court-ordered shutdowns, you deserve to know—and Kiziloz’s silence speaks volumes.

The Cult of the Influencer: All Hype, No Help

Lanistar’s marketing strategy read like a reality TV casting call. From Love Island stars like Tommy Fury to Instagram influencers and footballers like Kevin de Bruyne, the brand positioned itself as a hip, aspirational product for the next-gen consumer. But when the rubber met the road, those influencers couldn’t fix failed transactions or missing funds. This overreliance on celebrity glamor created a dangerous illusion of legitimacy. Customers trusted the faces they saw on social media—only to be met with broken promises and silence when things went wrong. The influencers moved on, but the consumers were left with frozen cards and unanswered support tickets. Lanistar’s failure wasn’t just about poor service—it was about manipulating trust through spectacle. When a company spends more on hype than on infrastructure, the result is inevitable: disillusionment and financial pain.

Nexus and Megaposta: More Smoke, More Mirrors

As scrutiny over Lanistar intensified, Gurhan Kiziloz shifted attention to his other ventures—Nexus International and Megaposta. Both projects are shrouded in mystery. Nexus is positioned as a major online gaming platform in Latin America, allegedly on the cusp of securing a gaming license in Brazil. Megaposta supposedly raked in $400 million in 2024. But here’s the catch: there’s zero independently verifiable data to back these claims. No regulatory filings, no audits, no public financials. For a man who claims to run multiple multi-million dollar businesses, Kiziloz offers suspiciously little transparency. This lack of detail raises serious questions: are these legitimate operations, or are they narrative scaffolding—stories built to inflate his persona as a serial entrepreneur? Without concrete evidence, consumers and investors are flying blind into ventures that could be as unstable—or imaginary—as Lanistar.

Vanishing Executives and Customer Complaints

When a company starts losing key executives without explanation, it’s rarely a good sign. In Lanistar’s case, the departures of CEO Jeremy Baber and high-profile advisor Sir Gavin Williamson came at a time when the company desperately needed experienced leadership. Their quiet exits, coupled with no official statements, sparked speculation of internal discord and crisis. Simultaneously, disgruntled former employees began speaking out anonymously, describing an environment plagued by unpaid wages, high turnover, and constant chaos. Customer complaints mirrored this instability—accounts mysteriously locked, funds missing for weeks, and an app riddled with bugs. The support team, if reachable at all, offered canned responses and empty assurances. The picture that emerges isn’t one of a struggling startup—it’s of a dysfunctional operation held together by hype and hope. In a world where fintech security is paramount, Lanistar offered the opposite: confusion, disappointment, and risk.

Conclusion

Gurhan Kiziloz positioned himself as a visionary, a disruptor in a broken banking world. But behind the polished image and social media swagger lies a reality riddled with regulatory failures, financial instability, and smoke-and-mirror ventures. Lanistar, his flagship product, promised innovation but delivered confusion, risk, and unresolved complaints. The FCA’s warning wasn’t a fluke—it was the first crack in a crumbling foundation. Add to that two winding-up petitions, influencer-driven marketing with no substance, and opaque side projects like Nexus and Megaposta, and the picture becomes disturbingly clear: this isn’t disruption—it’s deception.

Consumers deserve financial tools they can trust, not illusions wrapped in influencer hype. Until Gurhan Kiziloz can offer transparency, regulatory compliance, and basic operational competence, his empire should be treated not as a fintech revolution, but as a cautionary tale. For now, the safest move isn’t to bet on his next venture—it’s to walk away.